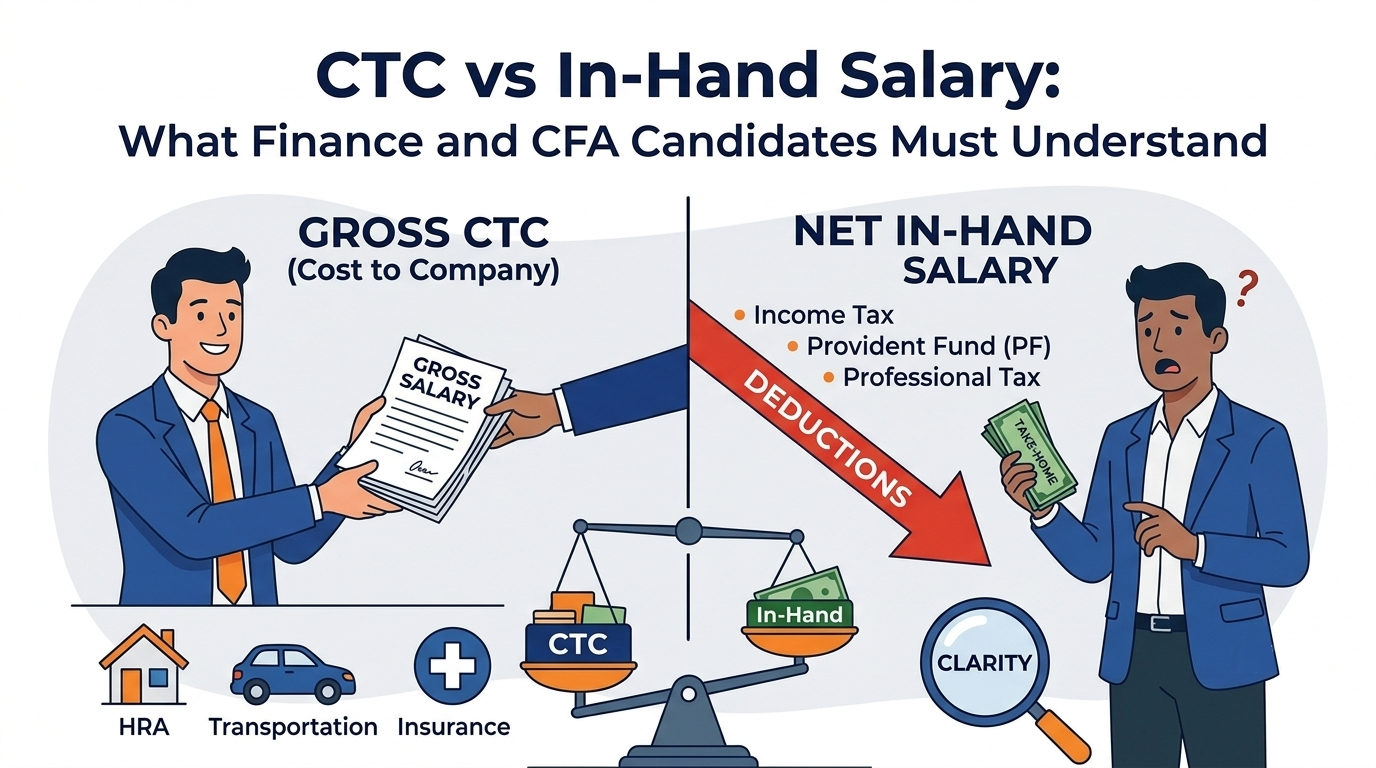

In early finance careers, compensation conversations usually begin and end with one number: CTC. It is the figure that appears largest in the offer letter, the one recruiters quote most often, and the one candidates tend to compare first. But CTC is not the money that actually reaches your bank account. It is the employer’s total annual cost of employing you.

That distinction matters far more than most candidates realise. For finance students and CFA candidates, the real question is not how large the headline number looks, but how much of it is fixed, how much is variable, and how much is truly available to spend, save, and use for exam preparation.

Key Takeaways

- CTC reflects the employer’s total cost, not the money you take home.

- In-hand salary determines your monthly financial reality.

- Two offers with the same CTC can produce very different take-home pay.

- Variable pay, bonuses, and employer contributions can inflate CTC without improving liquidity.

- For CFA candidates, monthly cash flow affects exam timing, study bandwidth, and stress levels.

- The best way to compare offers is to focus on fixed cash, deductions, and role quality, not just the headline number.

A role with a higher CTC can still leave you with weaker monthly cash flow than a lower-CTC offer if the structure is loaded with deferred benefits, employer-side contributions, and performance-linked pay.

That is why misreading an offer letter is one of the most expensive early mistakes in finance hiring. The difference between CTC and in-hand salary can shape your budgeting, your CFA journey, and even the kind of roles you can realistically accept early in your career.

The Three Numbers That Matter

Most candidates confuse CTC, gross salary, and in-hand salary because these terms are often used loosely during hiring conversations. They are not the same thing, and once you understand the difference, offer letters become much easier to evaluate.

CTC

CTC, or cost-to-company, is the total annual cost the employer incurs for hiring you. It can include basic salary, allowances, bonuses, employer provident fund, gratuity provisions, and certain benefits.

CTC is a cost metric. It tells you what the company spends, not what you receive.

Gross Salary

Gross salary is the amount before deductions. It is usually made up of basic salary and allowances, and may also include some bonus components depending on the company’s structure.

Gross salary is closer to actual pay than CTC, but it still does not reflect the amount that lands in your account.

In-Hand Salary

In-hand salary, or take-home pay, is what gets credited to your bank account after deductions such as employee provident fund, professional tax, and income tax.

This is the number that matters when you are deciding your monthly budget, your savings rate, and how comfortably you can handle recurring expenses such as rent, commute, food, and CFA prep costs.

Info:

Curious how much a CFA can earn? Check out our CFA Salary Calculator to get detailed insights.

What Sits Inside CTC

Offer letters in finance often look simple on the surface and complicated once you unpack them. The headline number is easy to understand. The structure underneath is where candidates often get misled.

A typical CTC package can be broken into four broad buckets.

Fixed Cash Components

This is the portion of compensation you can rely on each month. It usually includes basic salary and fixed allowances, and it is the part that should anchor your budgeting.

If you want to know whether an offer is genuinely comfortable, this is the first number to check. Fixed cash determines whether you can plan your life with confidence or whether you will be waiting for bonuses and reimbursements to fill the gap.

Employee-Side Deductions

These are the amounts reduced from your gross salary before you receive your take-home pay. Common deductions include employee provident fund, professional tax, and income tax.

Employee PF reduces monthly cash flow even though it supports long-term retirement savings. Professional tax is small but recurring, and it varies by state. Income tax can be the largest deduction depending on your salary band and tax regime.

These deductions matter because they reduce liquidity. A candidate who mentally divides CTC by twelve often overestimates how much money they will actually receive each month.

Employer-Side Contributions Included in CTC

This is where many candidates are surprised after joining.

Employer provident fund contributions are often included in CTC, but they do not come to you as cash. They go into a statutory savings structure instead. Gratuity may also be shown as part of CTC, but in most cases it is only a provision, not a monthly payout.

These items are real benefits, but they are not spendable income. They improve long-term security, not monthly flexibility. If you are comparing offers, they should be treated as benefits, not as money you can use freely.

Variable Pay and One-Time Components

Variable pay includes performance bonuses, joining bonuses, incentives, and other components that are not guaranteed every month.

This is the part that often makes CTC look more attractive than it really is. A package with a large variable component can appear stronger on paper while delivering much less predictable cash flow in practice. That matters especially in the first year, when you are still building financial stability.

For comparison purposes, variable pay should be treated as upside, not as base income.

A Practical Example

Consider a ₹10 LPA offer.

On paper, that number looks straightforward. It sounds like ₹83,333 per month. But that is not what most candidates actually receive.

A simple breakdown might look like this:

- Basic salary and fixed allowances: around ₹6.0 lakh.

- Employer PF and gratuity provisions: around ₹1.2 lakh combined.

- Variable pay: around ₹2.8 lakh.

Now subtract employee PF, professional tax, and income tax. Depending on the structure and tax regime, monthly in-hand salary may end up closer to ₹42,000 to ₹50,000.

That gap is the reason CTC can be misleading. The headline figure is not wrong, but it is incomplete. If you do not understand the structure, you may think you are comparing one salary when you are really comparing two very different cash-flow profiles.

Info:

Check our blog on CFA Salary in India to know more about estimated salaries and figures for CFA jobs.

How to Read an Offer Letter Properly

The most reliable way to evaluate an offer is to request the salary breakup in writing and focus on the cash portion first.

Before you accept any finance role, ask these questions:

- What is the monthly gross salary, excluding variable pay?

- How much of the gross is the basic salary?

- What is the employee PF deduction each month?

- What employer PF contribution is included in CTC?

- Is gratuity included, and how is it provisioned?

- Is professional tax deducted, and which state payroll applies?

- What portion of CTC is fixed versus variable?

- When is variable pay paid, and is it guaranteed or performance-linked?

- Are reimbursements paid as cash or as bill-based claims?

- Does probation affect variable pay or benefits?

These questions matter because two offers with similar CTC can produce very different take-home salaries. In finance hiring, the difference is often not in the title of the role but in the structure of the compensation.

Why This Matters More for CFA Candidates

For CFA candidates, monthly cash flow is not just a budgeting issue. It affects the pace of the entire journey.

CFA preparation comes with exam fees, registration costs, study material expenses, and the time cost of balancing work with preparation. If your take-home salary is too tight, even a decent-looking offer can make the exam cycle harder to manage. In that situation, the “better” offer on paper may actually be the worse offer for your career path.

A lower-CTC role with higher fixed cash can sometimes be the better choice if it gives you the breathing room to prepare properly, stay consistent, and avoid unnecessary financial stress. That is especially true in the early stages of a finance career, when your learning and exam decisions are still compounding.

The right question is not simply, “Which offer is bigger?” It is, “Which offer gives me the cash flow and stability to keep moving forward?”

How To Compare Offers Across Five Lenses

CTC should never be the only comparison point. A good offer is usually the one that performs well across multiple dimensions.

| Lens | What to Compare | Why It Matters |

|---|---|---|

| Monthly in-hand | Predictable take-home after deductions | Determines your actual spending and saving power |

| Fixed vs variable mix | Share of guaranteed pay versus performance-linked components | Higher variable pay increases uncertainty |

| Role learning curve | Exposure to valuation, credit, reporting, or analytical decision-making | Drives long-term skill growth |

| Brand and team quality | Nature of work, mentorship, and team reputation | Shapes future mobility and exit options |

| City and cost of living | Cash retained after rent, commute, and essentials | A salary goes much further in some locations than others |

If one offer is clearly stronger on at least three of these lenses, it is usually the better decision even if its CTC is lower. That is a more realistic way to think about compensation than chasing the biggest number in isolation.

Common Mistakes Finance Candidates Make

Treating employer PF and gratuity as cash

These items appear inside CTC, so many candidates instinctively count them as part of their salary. But they do not improve monthly liquidity.

Fix: Treat them as long-term benefits and compare offers using actual take-home cash.

Ignoring taxes and deductions

Professional tax is small, so it is often ignored. Income tax is much larger and becomes increasingly important as salary rises.

Fix: Estimate deductions before you build your budget, not after you join.

Assuming bonuses are guaranteed

Variable pay sounds attractive during hiring conversations, but it is rarely as stable as fixed salary.

Fix: Ask whether the bonus is guaranteed, performance-linked, or conditional on tenure.

Accepting an offer without a written breakup

Verbal salary explanations often sound better than the final payroll structure.

Fix: Always ask for the full breakup in writing before you accept.

Comparing only first-year compensation

A role with slightly lower cash in year one may give you better skills, better brand value, and better future growth.

Fix: Use take-home as the baseline, then assess the role’s long-term learning value.

A Better Way To Think About Compensation

A finance candidate should look at compensation the way a finance professional looks at any cash flow problem.

A headline number is never enough. You want to know what is guaranteed, what is delayed, what is conditional, and what is actually usable. That is true in valuation, budgeting, and offer evaluation.

The same logic applies to your first role. A salary that looks impressive on paper can still leave you underfunded in practice. A smaller package with stronger fixed cash, better learning, and more predictable take-home can often be the smarter move.

That does not mean you should always choose the lower-CTC role. It means you should stop treating CTC as the final answer.

Conclusion

CTC is a useful employer metric, but it is a poor decision tool for candidates. In-hand salary determines your monthly stability, your ability to study, and your ability to manage the real costs of early career life.

For finance and CFA candidates, the best offer is not always the one with the highest headline number. It is the one that gives you the right mix of fixed cash, manageable deductions, useful learning, and long-term growth. Once you learn how to read compensation properly, you stop being impressed by large numbers and start making better decisions.

Info:

Get started with CFA Level 1 or fill out the form below to get a career consultation.

FAQs

Q: What is the difference between CTC and in-hand salary?

A: CTC is the total cost a company spends on an employee, while in-hand salary is the amount actually credited to your bank account after deductions like PF, tax, and professional tax.

Q: Why is in-hand salary lower than CTC?

A: In-hand salary is lower because CTC often includes employer PF, gratuity, bonuses, and other benefits that do not come to you as monthly cash. It also gets reduced by employee-side deductions and taxes.

Q: How do I calculate in-hand salary from CTC?

A: You can estimate it by removing employer-side benefits, then subtracting employee PF, professional tax, and income tax from gross salary. The exact figure depends on the salary structure and tax regime.

Q: Is employer provident fund included in CTC?

A: Yes, employer provident fund is commonly included in CTC, but it is not part of monthly take-home pay. It is a long-term benefit rather than cash you can spend immediately.

Q: Which matters more when comparing job offers: CTC or in-hand salary?

A: For budgeting and monthly expenses, in-hand salary matters more because it reflects the money you can actually use. CTC is still useful, but only when you also check how much is fixed, variable, and benefit-based.

Q: Why should CFA candidates care about salary structure?

A: CFA candidates should care because exam fees, study material, and preparation time all depend on cash flow. A higher CTC may still be a worse choice if the take-home pay is too low to support your CFA journey comfortably.